|

|

|

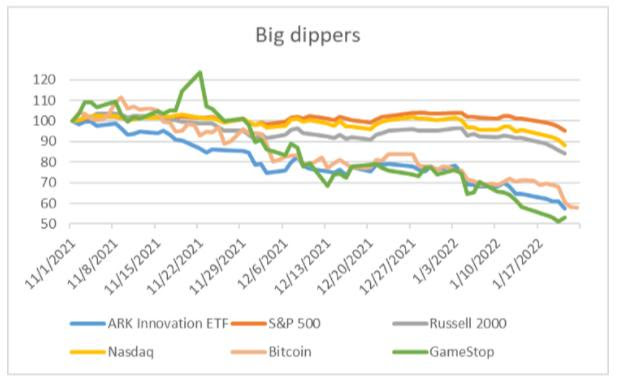

How scary is this?Risk assets have gotten hammered since November, with more volatile, high beta, speculative stuff taking the worst of it. Because the hardest-hit bits of markets are also some of the highest-profile — Cathie Wood’s ARK Innovation ETF, meme stocks, crypto, and so on — this may be making the situation feel worse than it is:

On a longer horizon, while equities are clearly going through an ugly patch, they are still sitting on big gains since the pandemic began:

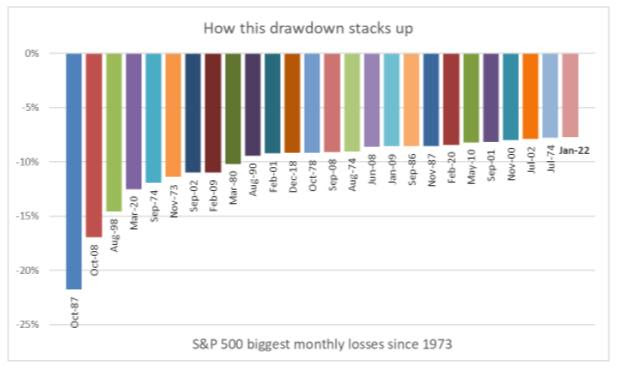

The decline thus far in January is not a big standout, historically (we looked back to 1973):

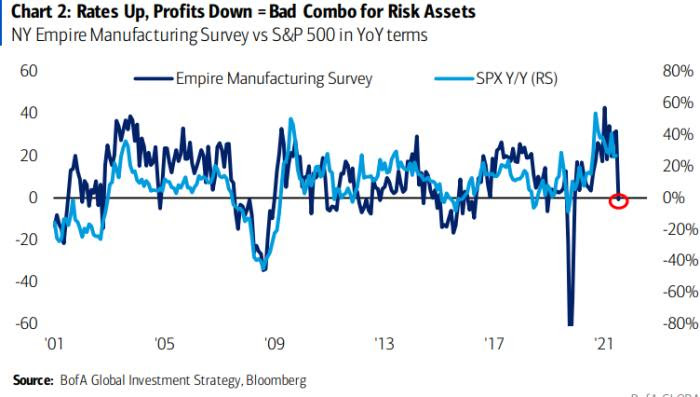

Admittedly, the policy, economic, and valuation backdrops are not particularly reassuring. We are heading into a rate increase cycle and the shrinking of the Fed’s balance sheet. The fiscal stimulus of the past few years is disappearing into the rear view mirror. While high inflation is currently matched with high growth, the inflationary aspect has control over consumer sentiment, which remains weak. Asset valuations are very high, which means long-term returns are likely to be low over the long term. There is clearly the makings of a bear case here, and Bank of America strategists Michael Hartnett and Savita Subramanian duly make it, in twin notes. Hartnett sees a one-two punch coming for equities. With the Fed hiking into a richly valued market, a “rates shock” will hit first, followed by a “recession panic” as growth expectations slow. He thinks the growth decline has begun already, pointing to this chart of S&P 500 returns tracking the New York Fed’s survey of manufacturing conditions:

Why a sequence of two shocks rather than one big jolt? In Hartnett’s words, We believe “rates shock” is just beginning and rate expectations too low . . . stocks, credit & housing markets have been conditioned for indefinite continuation of “Lowest Rates in 5000 Years” might only take a couple of rate hikes to cause an “event”. Wall Street leads Main Street hence our view that “rates shock” causes “recession fear”. Subramanian argues that with the Fed withdrawing support, consumers and firms lack the cash to keep buying equities at current valuations: Healthy balance sheets are unequivocal positives for consumption, business investment, and thus for the economy. But can consumers and corporates act as white knights and support asset prices via continued equity investments and buybacks? We’re sceptical. Cash relative to S&P 500 market cap is near record lows . With [Fed] balance sheet reduction of over $600B in 2022 (house view), corporates are more likely to see the negative impact via a rising cost of capital and asset deflation, than the consumer will. Her key chart:

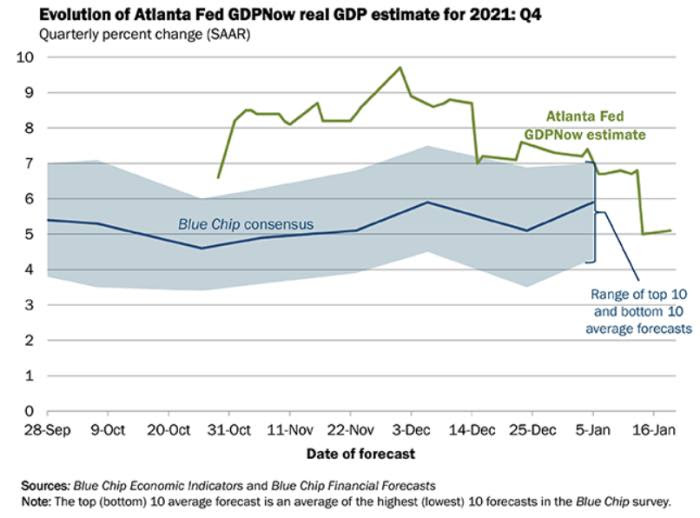

Hartnett and Subramanian are calling for a down year in equities, not a crash. But even so, we read less into the recent wobble in the economic data, and into the Fed’s positioning and intentions, than they do. Yes, there has been a flurry of poor growth data: not just the Empire State survey, but increase in jobless claims, and a weak December retail sales report. The resurgence in energy prices makes it all look worse. The Atlanta Fed’s estimate of Q4 GDP tells the tale — growth estimates have come in sharply over the past month:

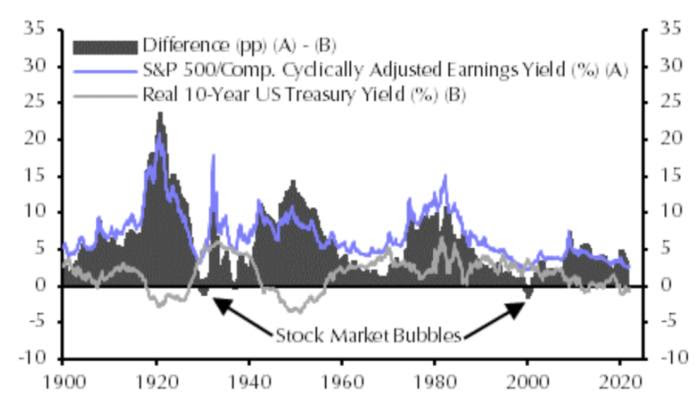

A combination of an inflation-driven tightening cycle and a growth slowdown is indeed less than appetising. But note two things. First, we are still looking at pretty strong real GDP growth. We are still solidly in growthflation rather than stagflation territory. Second, while growth is slowing recently, until we know how much of the slowdown is due to Omicron, it is probably best not to overreact. The big question for this year remains the same as it was a month ago: does Omicron loosen its grip on the world economy, moving demand away from goods and back towards services, cooling inflation a bit, so the Fed can tighten at a stately rather than a panicked pace? The answer may still be yes. The best argument against an equity crash remains the same, too. It is that bond yields are still far enough below earnings yields that a great rush out of stocks seems unlikely. Oliver Allen of Capital Economics provides this graph of the difference between the S&P 500 earnings yields (that is, the earnings/price ratio) and 10-year Treasury yields, which shows this measure is still far from the danger zone:

This is a scary moment. Market corrections and shifts in policy regimes are scary. But it does not look like the edge of an abyss, either. (Armstrong & Wu) |