I’m speaking at the Pension and Benefits UK Show on July 1st on whether fees matter more than value. I’m going to be arguing that, for consultants, fees matter more – because we can do something about them.

But while total return matters most, it’s not something we can control, most return is market driven and none of our business.

Am I right?

My friend and colleague, Emmy Labovitch (she what wrote the stuff that the FCA published this week) says that she has moved on and that the world is now about educating people to understand value rather than just stamping on fees.

I don’t get why she says this (as she just stamps on unwanted fees like cockroaches in a kitchen). I think she is a school teacher and every time I agree with her, she decides its time for the next lesson!

Should I fight?

It may be that she will be in the audience. If no-one rises to Jonathan Stapleton’s challenge and steps into the ring against me, she may even be my opponent.

The idea of the session is to test on the audience, the debate about where investment consultants can add value. Is it in getting a reluctant public engaged in getting asset allocation right, or is it in protecting the general public against rip-off charges and costs (as they are generally known).

Of course , being told I’m wrong by Emmy – the old school head girl, is not something that I’m having anything of. I am busy marshalling my arguments and honing my attack.

Are the numbers are with me?

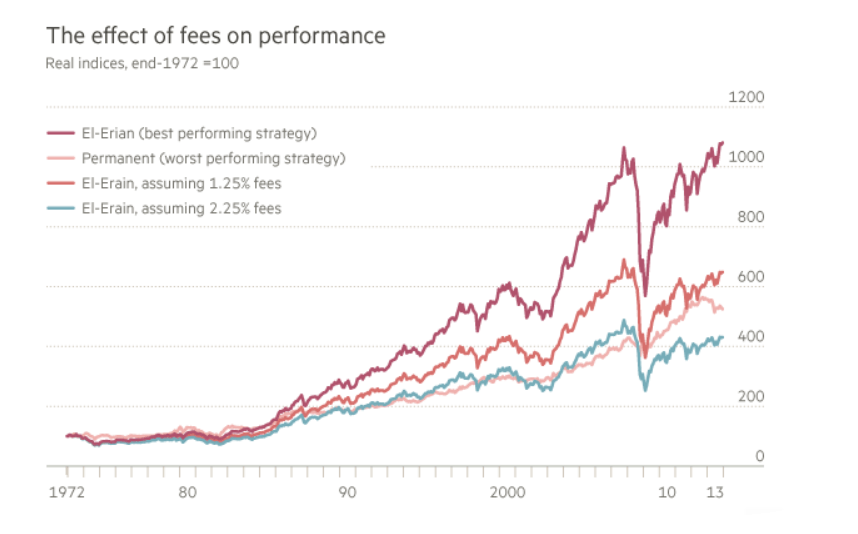

So I am pretty pleased to find John Authers publishing an article in http://www.ft.com (get yourself a subscription) that shows quantitatively that the differences over 30 years between certain famous model portfolios were as nothing (in terms of member outcomes) against the impact of halving the fees in each portfolio.

Advisers advise, fund managers manage

My argument is a simple one. Fund managers manage funds, advisers keep them honest. If advisers concentrated on keeping fund managers focussed on member outcomes by ensuring they managed costs, fund managers would do a better job.

But if advisers feel their job is to manage funds, they should become fund managers and stop managing funds.

I think we need well-advised well managed funds but I don’t think you can do both jobs at the same time without having another adviser keeping you honest.

Cost control is not the only job of an adviser

This is not me saying that an adviser should be so unambitious as to give up on the business of value altogether.

I, nor First Actuarial, are not so dumb as to dismiss the search for alpha (or even smarter beta) in the relentless assault on fees.

Clearly there are some fund managers who make sense of the markets better than others, and whether through their assessment of stocks or of sectors or of asset classes, can add value.

And pointing people to good managers and away from bad managers has to be within the adviser’s brief…

As well..

But as the chart shows, advisers who had chosen managers with low cost bases would have added more value than advisers who had chosen the right manager at the wrong price.

Which is more or less what I would argue against anyone who stood up and said the job of the investment consultant is to find the right manager or to manage portfolios of managers to get the right mix of managers and asset allocation or any more complicated role than that!

We have, collectively failed to bring the cost of intermediation down below 2%pa over the past 150 years (see blogs passim). By intermediation, I do not mean just the cost of advice, but the cost of the chain of people who interfere with the direct investment of your money- lawyers, custodians,advisers, brokers,dealers, managers etc.

I see the biggest challenge to our generation of investment consultants is to do better than the previous five, whether we can use technology to disinter mediate and to halve the costs within the portfolio.

But you might think differently….

So here’s the challenge to you.

1. Get yourself a ticket to Pension and Benefits UK 2015.

2. If you want to challenge Tapper, get in touch with Milly Sheehan by email with the header “I want to challenge Taps” milly.sheehan@incisivemedia.com

3. Whether on the rostrum or from the audience, turn up to the session which is in the afternoon of July 1st (QE2 Conference Centre)

4. Have your say and tell me that I’m wrong!

5. Influence the audience and win the vote!

Surely advisers should be concerned about both asset allocation and fees; one does not need to make a choice. Advisers should also be careful what they wish for. Henry Tapper says “Fund managers manage funds, advisers keep them honest”. So who does he think is keeping the advisers honest?

I hope that trustees, employers and advisers will only pay fees to consistently honest advisers, but it’s the Regulators who keep advisers honest day to day! Don’t they?