Ladies and Gentlemen, here’s the new buzz phrase, direct from the US of A.

“To and through” retirement strategies simply lengthen the horizons of the investment managers from an arbitrary end point – (the fixed or selected retirement age), to the point where money is last needed (death).

Morbid as it sounds, it is the unique feature of pensions(as opposed to ISAs for instance) that it seeks to insure against living too long.

Predicting how an individual will spend money in retirement is a mug’s game, though studies of large numbers (Bristol University has recently surveyed 20,000 Brits in retirement) can allow us to generalise. So we hear consultants now talking about the “U-curve” of spending (as if they were experts).

Overlaying general behaviour onto individual circumstances is of course what happened when it was prescribed people had to annuitise their retirement savings from money purchase pots. It didn’t work and nor will over dogmatic products that require people to have income paid to them as some academic, fund manager or insurance company deems fit.

In this sense, the idea of collective DC is stillborn. Individuals will have to have the capacity to spend their cash as they wish and if that means turning up the spending beyond recommended limits so be it. If I drive my car at 7000 RPM for long periods I will burn out the engine and the same will happen to people who overspend in the early years.

But in another sense, collective DC is very much alive. A general fund which people participate in ,have specific rights to which is managed for “people like you” has great advantages over an individual “drawdown” arrangement.

Elsewhere we have referred to such funds as “target pensions” as they allow those within them to target certain levels of income with a higher degree of certainty than they could were they simply investing on their own. The wins are about economies of scale and the capacity of fund managers to do clever things like cap volatility and/or use dynamic asset allocation to reduce the chances of you running out of money.

To use the parlance of the IFA, to prevent “pounds cost ravaging”.

Of course we would be very silly indeed to suppose that the current average private pension savings of around £30,000 is going to be much of a factor for those retiring today, the basic state pension, if paid in full is worth around 6 times that and compared to the value of the in retirement housing stock, there is as much money again in people’s personal wealth. Add to this ,people’s personal earnings capacity and you can start constructing graphs like this (from Kevin Westbroom of Aon)

Or construct fantasy retirement strategies like the one below

All this is by way of a prologue to the main course of today’s blog, which is a lesson I was taught by a clever man who runs one of the largest DC funds in the UK.

He didn’t do the research, it was done by an investment house in the US called GMO Wooley, but he introduced me to the phrase “to and through” and he is the first non-professional DC pension trustee I have met, who has a stated aim of providing a means for people to spend their DC savings.

Here’s how the yanks explain it…..

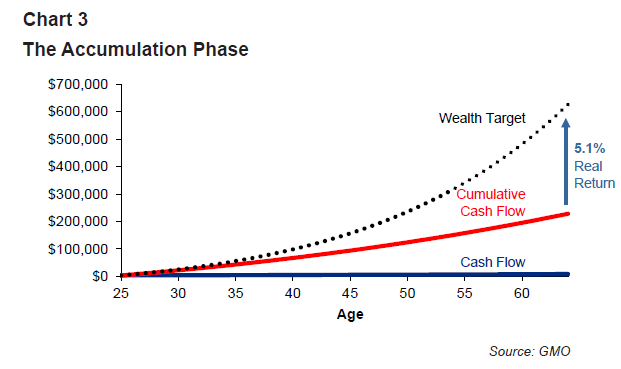

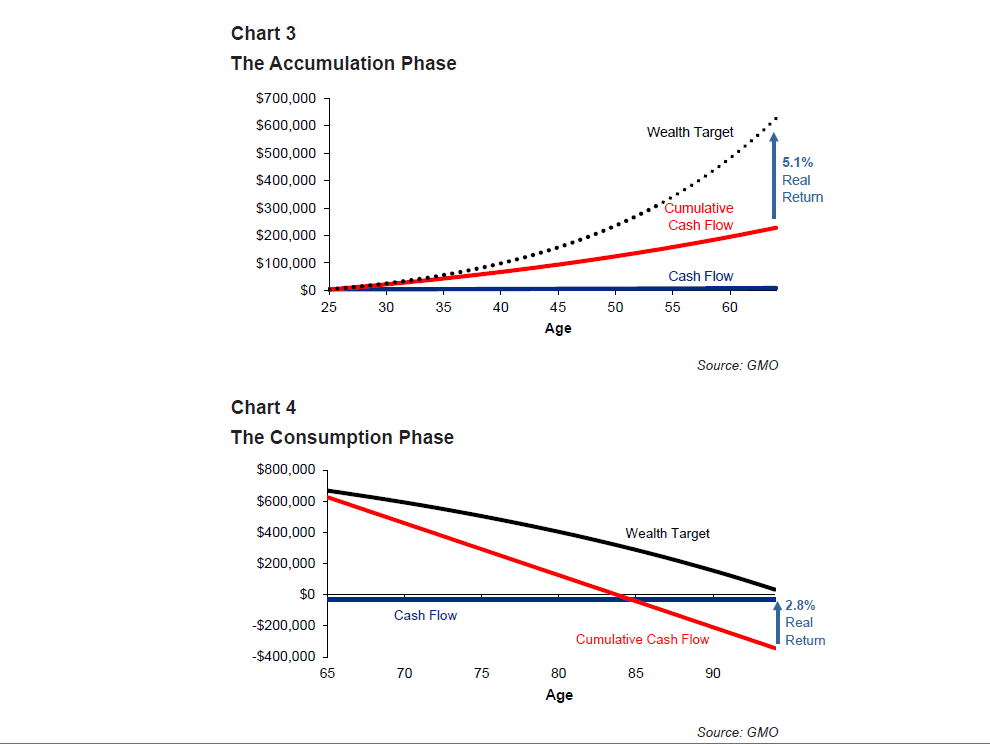

We start with a wealth target- the amount of money we hope to have to meet our post retirement needs. Frankly we live in hope, in this example we are hoping that our savings get a real return (eg beat inflation by) 5.1%, because we’ve worked out we’ll need $650k or thereabouts

{kind=link}

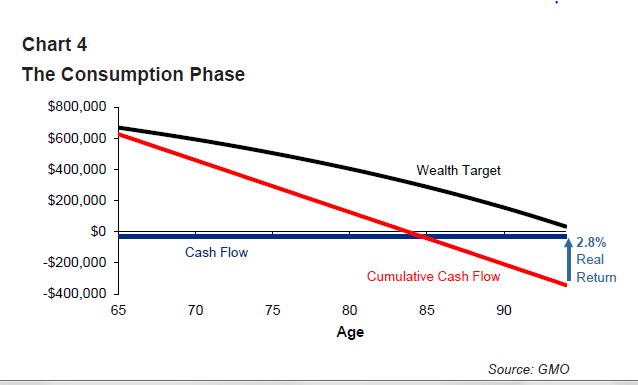

What follows is the spending of the money (or consumption) as the boys from GMO have it. The red line is what happens if you just spend from a bank account (without interest and the black line shows what happen if you consistently got 2.8% more than inflation on your money (being a bit more cautious as you are in spending mode)

So once you’ve marched up to the top of the hi, you now have to march down again

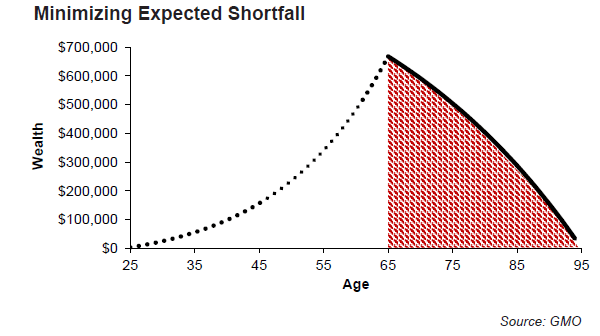

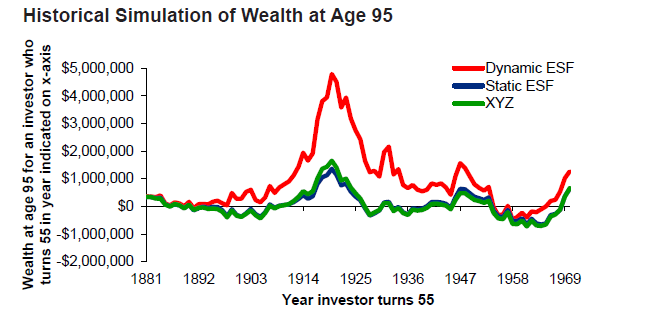

And if you put the journey up and the journey down together, you get a picture that looks like this.

If anyone’s climbed a mountain, they’ll know that you have to take more care on the way down than on the way up, the injuries happen when you are descending and lose control.

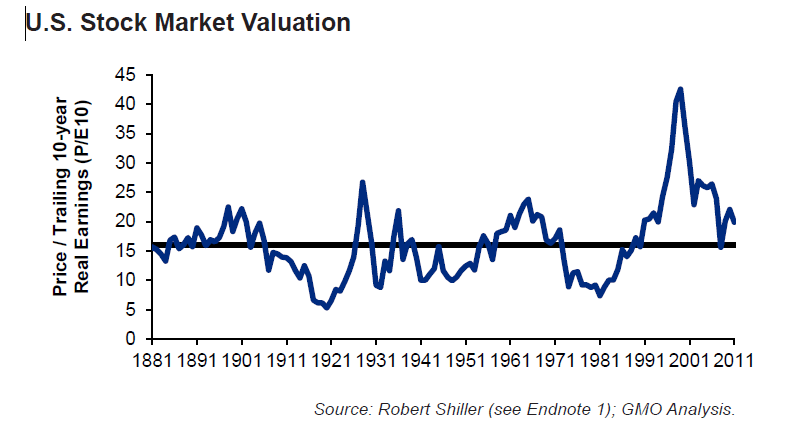

The graph below shows you why financial injuries happen.

If you take some money out when you are above the black line, you’re laughing! If you take money out when the blue line is below the black line you are “pounds cost ravaging. So how do you find a way to minimise the times when you are below the line. If you are Schroder you run with a variable volatility cap, if you are these guys you show things by turning things on their head.

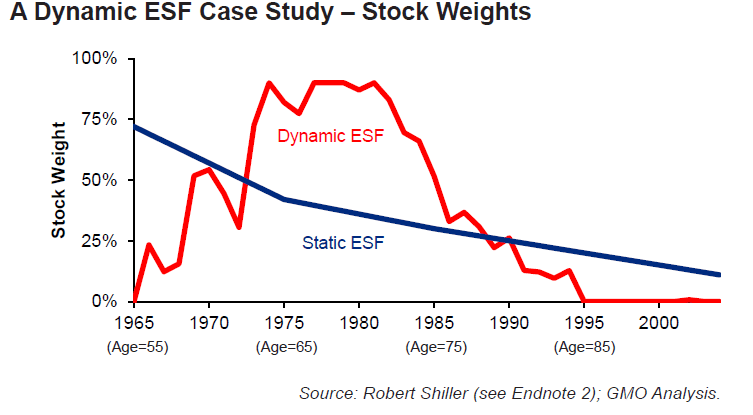

Dynamic ESF (Estimated short fall) prevention, is simply a technique where you are investing in things which do the opposite of equites when equities are doing badly and equiies rather than other things when equities are doing well. The timing is of course critcal and you shouldn’t try this at home.

What this graph shows that you should have owned loads of

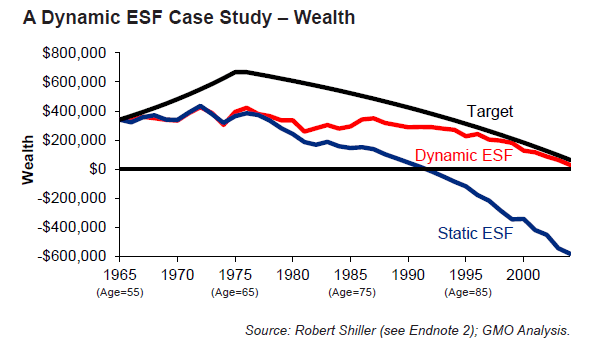

So by adopting this nifty investment strategy, you get to $0 a lot later and shouldn’t run out of dosh until you’re old enough not to know what to spend it on. (red line for the lucky dynamic investor)

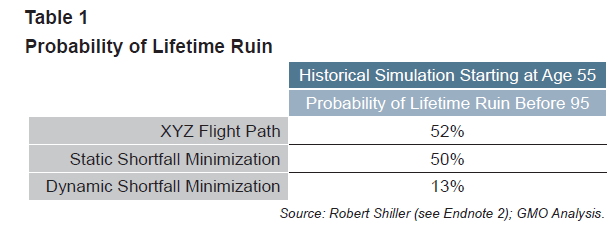

“Liftetime runin” is a charming phrase the yanks have dreamt up to describe what it’s like when your money runs out.

But it’s a useful phrase to focus the mind on the acceptable level of risk someone is prepared to take with their savings.

My wise friend Morten Nilsson, pointed out to me that we live with uncertainty over our income all our working lives, the only time we demand certainty is from our annuity when it becomes a holy grail.

Simulations of the model that Shiller & Co have produced going back to the 19th century suggest that even if their ESF strategy was in place, ther would still be periods (most noticeably around 1950 when people would have run out of money by 95.

Ask yourself, could you handle that risk? If not, you might be asking yourself how much of a haircut would you take on your later life income to get the certainty of a lifetime annuity (and when would you lock in?).

To and through strategies are about keeping you in real assets, earning real returns without jeapordising your later life lifestyle too much. No one says that this is as secure as an annuity.

Everybody still has the chance to buy an annuity at any time/

But if you asked your boss for a guaranteed job at a guaranteed wage for the rest of your career and he said the price would be a 50% pay-cut, I wonder if you’d buy into that level of certainty.

Let’s finish with those two graphs that show the to and through. I think you are going to see a lot more of them in the years to come!

This forms the basis of a presentation I will be giving at the Retirement Income Solutions Conference on 28th May. If you are going, I look forward to answering your questions and listening to why I’m wrong!

Otherwise there is always the comments box!

This article first appeared in http://www.pensionplaypen.com

{kind=link}

Interesting stuff Henry.

Perhaps I missed it but I did not get any sense of the pattern of expenditure assumed in retirement. There is a lot of research on the assets and their issues but less of the “liabilities” side of the question. It is of course complex – for a start any analysis of spending in retirement is linked to the assets available and expected to be available, which makes the analysis difficult.

Kevin’s diagram is a good pictorial simplification. But we need more work on behaviour changes as people age (for example on attitudes to bequests and spending on travel etc,), changing needs, attitudes to spending in the light of different mortality risk as people age, and the same to spending in the light of investment risk. And lots more.

There’s a danger we focus too much on the assets and not enough on the liabilities/consumption side of the problem, which I fear is a common problem in pensions.