There are those who thrive on the ups and downs of the stock market; high frequency traders take fractional advantage of moves up and down and like wind farms, make most when it’s stormy. You can buy and sell this volatility, using derivatives based on the Vix index (of volatility in the S&P 500 over the next 30 days).

For those who are saving, there is the comfort that when the market is down you buy cheap and when the market is up, what you bought cheap is “in the money”. Even when you buy “dear” , you don’t have to sell “cheap” because you are saving.

Savers needn’t be afraid of volatility, but spenders should.

Volatility is why most income drawdown plans don’t work as planned.

Unless, you are Paul Lewis, and invest your retirement pot in cash (forsaking any chance of investment returns), your money is in the market and the market is historically volatile.

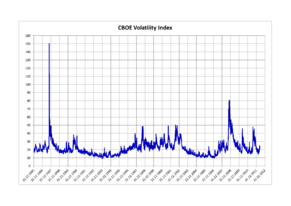

This is a chart of 30 day volatility on the American stock market 1985 to 2012.

You may not read the small print, but you get the big picture.The big spikes are where the market is all over the place and over the course of 27 years (around the lifetime of an average drawdown), your fund is going to get punctured by one of those spikes.

It’s not as broad as it is long.

The problem is asymmetrical, it does not have as many winners as losers. I presented this slide some time ago to explain why (thanks Alan Higham for the graph).

The spike in the volatility on 9th August 2011 wasn’t caused by anything rational, it was down to some problems with computers that screwed up valuations.

But the market had a field day. Those who could see what were going on and were able to trade were able to take advantage of those who had to trade but didn’t.

In short, hundreds of thousands of small investors (quite often people with money in drawdown cashing out to get their monthly payment) found themselves selling at a price 9% lower than at the start and end of the day.

Alan Higham’s internal statistics (when he ran Annuity Direct) was that over 70% of the money that was disinvested to buy a once in a lifetime annuity , was disinvested from the markets.

What this means is that a high quantity of those people buying annuities around the 9th August – sold shares on 9th August – many losing as much as 9% of their retirement savings.

And 9th August 2011 will go down as a day when nothing much happened, the markets started and ended the day at around the same levels.

Paul Lewis – right and wrong

Why Paul Lewis is both right and wrong is that he understands he is powerless to protect himself. As a single investor he has (as the slide above shows) no power to determine when he is disinvested and it’s not just sod’s law- it’s market forces, that dictates that he will get the worst price in the day for his disinvestment.

This is not paranoia, it is the law of the jungle. Individual investors are easy meat for high frequency traders. Infact without individuals wandering around in the jungle, there would be no-one for the tigers to eat.

But Paul is wrong to think his cautious approach is right for everyone. Paul is (I think) 67, my actuarial tables tell me he’s got another 20 years in him (and they are probably underestimating Paul!). If Paul stays in cash for 20 years, he will either get a pitiful amount of income or he will drawdown too fast and find himself cashless in his eighties. Paul says cash is no place to be for someone in his 60’s, I say (in general) he is wrong.

Back to the Great Fall of China

On Monday, the Chinese stockmarkets tanked, today they are on the rebound. The FTSE tanked on Monday and but on Thursday it had recovered all its losses and a little more. Like the 9th August 2011, the week of August 24rd 2015 may be remembered as one where nothing much happened.

But people who were selling their pension pots to pay off the mortgage – and did so at the start of the week – the amounts in their accounts could have been 5% more if they’d waited till the back of the week.

Who is to blame?

No doubt there is some ambulance chasing dingbat, opening up the back doors and wheeling out the stretcher as I type. Somebody is to blame for the Monday disinvestor being in shares, somebody to blame for him selling at the bottom of the market on Chinese Black Monday.

I can understand the disinvestor being peeved, he had no control. No one was looking after his interests, he was wandering around in the jungle on his own.

The problem with being in the jungle at night..

Some time ago we gave up on the idea of mutuality. The concept that held together our insurance companies, building societies, even banks – was that you were stronger together.

Part of the problem has been that idiots have been put in charge of the co-operatives, but the bigger issue is that we have been led to believe that given a good torch (and a financial advisor) you can get through the deepest jungle on the darkest night.

Forget it- I’ve been an advisor – advisors are no more likely to stave off a tiger than you are. Which is why sensible advisors have always suggested people club together to protect themselves from night-time jungle perils.

Until now that is.

Now it’s every man for himself. People with little or no understanding of the markets are drawing down from individual funds which offer little or no protection and many will be ruined.

Even people who drew down a slice of income early this week (from an equity based fund) will have upset the plans for the rest of the year, they’ll have sold too many units, their fund will be ravaged and the remaining units will struggle to get the plan back on par.

The ravaging for these people will be felt for years to come as their funds remain in deficit, only two things can happen – they must take a pension pay cut or risk running our of money.

Are collectives better?

You bet they are. collective drawdown arrangements (better known as CDC) have three key advantages

- They manage the risk of selling at the wrong time over thousands of people, some drawdown luckily , some unluckily but the lucky subsidise the unlucky and everyone gets something like what they expected – no nasty surprises.

- Collectively you can afford someone to manage the dealing on the fund so you are not always selling at the worst point of the day/minute/second. Collectively you have some clout in the jungle.

- Together, you can provide each other with protection against calamaties – living too long being the most calamitous happening for someone on their own. Collectively , “longevity” can be managed.

Where are the collective solutions?

The last great attempt to sort out retirement collectively – the defined benefit scheme – was scuppered by guarantees. People got too greedy and wanted all the risk transferred to the plan sponsors- the employers. Employers recklessly agreed. Government’s encouraged the greed and the recklessness.

The door slammed shut on DB plans when accountants introduced mark to market valuations and things could get a lot worse. If DB plans had to reserve for their guarantees as insurance companies do, then the deficits would be out of sight.

The collective solutions are in hiding – or perhaps in waiting. There are brave people- people like Kevin Wesbroom, Robin Ellison, Con Keating, David Pitt-Watson, Barry Parr and a few others who keep the flame alight for collective solutions.

There are many – many on social media – who want to extinguish the flame. In weeks like the one we’ve just been through, I realise that income drawdown is not the right plan for most ordinary people. They would be better off in a collective arrangement.

loser

winner

I’m going to make sure that the light does not go out and that the collective solutions to this problem continue to get publicity.

Henry – Savers should in fact be worried by volatility. The paragraph below is taken from one of my recent articles:”Consider the idea that volatility does not harm the long-term investor, who can ride this out. It is true that an investor with long-term liabilities, such as future pensions payable, may not be forced to liquidate holdings in times of market distress, but that does not mean that high market volatility is not harmful to long-term investors. The effect of this volatility is to lower the long-term compound rate of return achieved even though the asset has not been sold, and the volatility penalty is quadratic . With 10% volatility, a 5% arithmetic annual return will be realised as 4.5% compound and with 30% volatility, this will be just 0.5% – these are time average returns. Given this experience, long-term investors should be expected to be inherently cautious and conservative.”

Con

Mr Tapper, I’m Paul Lewis’s IFA and I look after his SIPP – I am intrigued as to how you know so much about it! Paul does, I realise, make no bones about his risk-aversion as far as “real assets” are concerned, but you don’t know the whole picture and maybe, just maybe, holding cash in his SIPP is appropriate in this particular circumstance. Best,

Mark

Paul Lewis @paullewismoney

@CashQuestions > drawdown isn’t problem it’s where fund is kept. My pension fund all in real cash and when I draw it so will drawdown be.

3:39 PM – 24 Aug 2015 · Lille, Nord-Pas-de-Calais, France

Retweets favorites

Paul may be right for Paul, but he has a vast following!

I would advise against those in their sixties avoiding real assets (unless they are about to draw the lot).

Where Paul is right is to draw attention to the problem and encouraging thinking on these issues. Thank goodness he is frank in his opinions.

Thanks for your comment

Henry, I think it would be good to explain how collective defined contribution works in future blogs in a less simplistic way. Whilst you explain the principles of it very clearly, and whilst you do not wish to blind us with actuarial science, is there a way you could educate those of us advisers who are interested in what you say but maybe do not know enough about the mechanics of CDC for us to be converted?