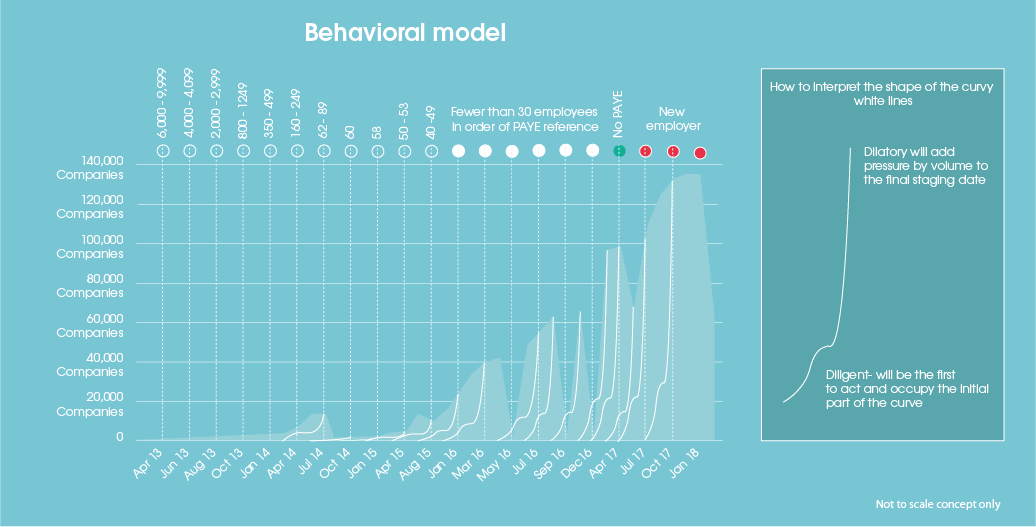

Over the past ten days, I’ve been tracking down members of the “pension congregation” prepared to test my “select a pension” tool that will feature on http://www.pensionplaypen.com. In case you aren’t up to speed, it’s all about creating capacity for employers hitting certain crunch points in the auto-enrolment staging process (see graph above).

Over the past ten days, I’ve been tracking down members of the “pension congregation” prepared to test my “select a pension” tool that will feature on http://www.pensionplaypen.com. In case you aren’t up to speed, it’s all about creating capacity for employers hitting certain crunch points in the auto-enrolment staging process (see graph above).

We’ve worked out that employers will be of two types; the majority will see auto-enrolment as a risk to their business, the minority will see it as a way to establish or improve their total reward to staff.

Some employers will be diligent in their approach and some will be dilatory. The diligent will heed advice to start planning early and will find the task of choosing a pension and implementing auto-enrolment relatively easy while those who are dilatory will struggle.

We learned this week that the Cabinet Office had in May issued an amber warning over the delivery of auto-enrolment, this seems to me to be about right. The jury is very much out as to whether sufficient momentum can be maintained from the succesful launch over the past twelve months (we kicked off in July 2012 though it’s only now that we are getting reliable data on how things are going).

But back to my testing program. I’ve had a great response. Nearly 100 people have put themselves forward. I was going through the list this morning and most are either advising big employers or working as pensions,payroll or finance experts looking to provide umbrella solutions for smaller employer. What is interesting is that most of them are actually employed by organisations that are small enough to be in the 2015-17 staging groups.

What I am hoping my testers can do, is to think through auto-enrolment not from an advisory standpoint but from the standpoint of a business owner. It’s one thing to talk to employers about their duties but another to consider how those duties will impact on your business plan.

It seems to me that for auto-enrolment to be a big win for Britain, we will have to shift the percentages around. At the moment, all the research I can get hold of suggests that auto-enrolment is viewed as “red-tape”, “business-risk” and a burden. There is no doubt it is all three.

However, the outcomes of auto-enrolment could, in a rose-tinted world be that staff are better rewarded ,better motivated and more productive knowing that they are working not just to pay today’s bills but tomorrow’s. Employers who can convince their staff that they not only do auto-enrolment but promote retirement saving within the workforce could be seen by staff and potential staff as progressive.

For this sea-change in employer attitudes to occur, we need to create a buzz about enrolling the workforce among employers. This is essentially what the “I’m in” campaign has kick-started, but it cannot simply come from the top-down. Government campaigns are unlikely to woo employers, anymore than the promise of a state owned pension solution. Both the DWP and NEST are doing great things but it is up to the private sector to create the kind of positive buzz around auto-enrolment that occurs in other areas of business.

There are plenty of success stories for British business to shout about, we have a strong service sector,a growing manufacturing sector and we have low unemployment. Relative to other European economies we are blessed with the freedom to take our own decisions and we have a stable and corruption free Government. Unions and employers work together better than at any time in my working lifetime and we have embraced new technologies so fast that we can adopt a complex notion such as auto-enrolment with a degree of confidence.

We have seen projects as ambitious as auto-enrolment work, most obviously in New Zealand (the closest comparator) but also in the Australian “Super” system. We have second mover advantage, learning from the first adopters and bettering their systems.

I have put as a strap on http://www.pensionplaypen.com a strap-line “restoring confidence in pensions”. I think I should take that down, it’s connotations are too negative. I think what http://www.pensionplaypen.com is about is “putting a buzz into auto-enrolment”. Of course, part of the work is in cutting out the undergrowth that has grown up over years of relative neglect, but it’s clear that the essential machinery needed to run auto-enrolment is in place, still working and indeed in rude health.

We should not minimise the impact of the employer duties, they are onerous and will be disruptive. But we must put them in the context of the greater good. The great infrastructure projects, the building of our canals, railways, roads and now our technology super-highways have not been built without cost. They cannot be justified by immediate return on investment. Many of these projects are delivering ROI 100 years after they were put in place.

This wider view of a public enterprise in which we are all in, is the only way that we can properly embrace the new pension system. In this context the £300m spent on NEST is not entirely wasted, indeed it may be seen as the seed capital for our new welfare system.

I’m going to take from this blog, the introduction for my 100 testers who I want to be champions not just of http://www.pensionplaypen.com but of the auto-enrolment process. Sure I want them to kick hell out of the tyres, but I want them to do so with a smile on their faces, knowing that if we can this site right, other sites will follow so that we can turn that amber light green.