Charlotte Clark – one of the architects of auto-enrolment and now head of private pensions in the DPW – is an economist. She is familiar with cost having worked in a corresponding position in the Treasury and it was she and her team who were responsible for the original costings for auto-enrolment published in 2012 by the DWP to justify the project.

I challenged Charlotte on these figures in a meeting of the Friends of Auto-Enrolment before the election, Charlotte confirmed that the DWP are revisiting these numbers in the light of experience. Her view was that the original estimates were “ball park right”, I am sceptical about that.

However, I am hopeful that small and micro firms may be able to stage for considerably less than the 103 man days of effort that the London Business School estimated staging cost, according to a joint study with Creative Benefit Solutions. I have written in the past to say that the £23,800 average cost estimated in this latter survey is as unhelpful as the low-side costings of the DWP in 2012.

There has been no academic work published on this subject of late, Dr Ian Clacher of Leeds University is currently looking for a sponsor for this project and perhaps Charlotte might talk with him about getting data from the private sector. I and other like mined individuals would be happy to help get a true estimate of the current cost of auto-enrolment. A finger in the air estimate would be that it costs an average employer staging today around £2500, but that figure needs to be tested (and I’d be grateful for any research that has been done on this subject.

There is a very interesting post on the LinkedIn Pension Auto-Enrolment Group. If you are in the group you can read the thread here. I won’t publish the entire thread here (as it is too long and many contributed to the members of the group alone), but I’m happy to publish my contribution

There are two areas where significant cost savings can be made. The first is in the cost of manually processing data transfer. There are two organisations- pensionsync and efileready which are working on providing the means for us to go file less. Whether their APIs integrate to and through middleware or directly to and from payroll and providers, it is likely that the leading providers (and lets hope Aviva are among them) are “going fileless” shortly.

The second area, mentioned in this thread, is the cost of advice. Delivering choice on workplace pensions has typically cost thousands of pounds, it is a research intensive process and with so much to consider- contribution rates/structures. payroll integration/member borne charges and the investment merits of the provider offerings, this continues to defeat most advisers.

So most employers are offering restricted panels or default offerings.Oddly we have capacity, this is not what people thought would happen, we have a number of providers but we don’t (yet) have the means to pass data to and from them efficiently and we have no way to assess their various merits.

Of course, you know what’s coming! Pension PlayPen is the first- and hopefully not the only – way to choose a pension on-line.

Others such as Financial SatNav and defaqto are following us in creating digital advisory systems. I hope there will be more.

We’re integrating our service with pensionsync, and will integrate it into the services offered by advisers and payroll software providers. If we can get data integration right, we can bring our price down so that choice can be a “no-brainer”.

PAPDIS is the foundation for all this, not only is it a file format in its own right, but it is the template for doing everything else. It will not be universally accepted, but it is the means for many new entrants to get a market foothold and to compete with existing players- being PAPDIS ready is a serious advantage to the new providers.

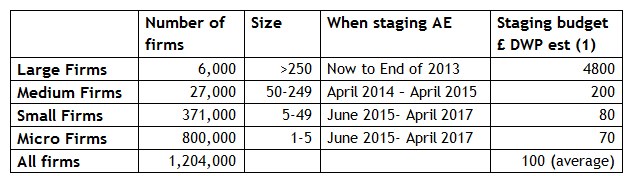

A note to Steven and Simon – from 2018 onwards, there are (according to tPR) 200,000 newcos staging each year.That’s four times as many as will stage in 2015!

Many will start on primitive software and some will migrate and become the Vodafones and Microsofts of tomorrow! Wherever you are positioned in the market, we hope that you will encourage better data integration with your entire range of products (Cloud or Desktop) and that you will encourage the use of digital technology to help employers make meaningful and informed choices.

Payroll is key, and a constructive attitude on these two issues, is key to the success of auto-enrolment not just over the next three years, but well into the future.

It is very hard to stand in the way of technology. The use of the web to deliver efficiencies is evident in all walks of life. Just walk down any street in the country and you can see people conducting their affairs using precisely the kind of technologies that I mention above.

There is resistance to these technologies among advisers, payroll intermediaries, payroll software providers and pension providers. The resistance comes from the cost of change. So long as these participants resist change, their costs will remain high and eventually they will lose business to those who embrace change and can bring their costs down.

The difficulty, as ever, is in investment. In order to be competitive , you need to invest in technology , re-design systems and processes and accept that the way you made your money in the past has gone.

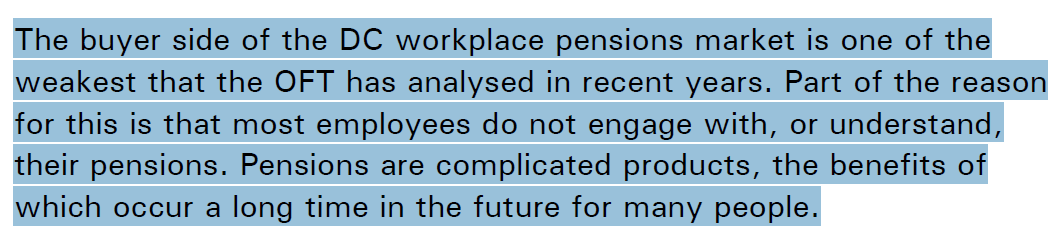

I am confident that auto-enrolment will become cheaper. But I hope that it will not achieve cost savings by taking short-cuts that cut out the engagement of employers and employees in understanding the need to contribute more and invest wisely for the future. As the OFT report stated

Auto-enrolment is going brilliantly well, when Ros Altmann has got her feet under the desk, I hope that she will encourage us to drive forward these technological advances to ensure it moves to the next stage, the staging of the mass of employers, with confidence.

We must bring the cost of choice down, we must bring the cost of data integration down. We must make the provision of investment services even better. Above all we must restore confidence in pensions.

When we have people’s confidence in the pension schemes we use and employer’s confidence that auto-enrolment is an enhancement not a drag on the business, then we will see people wanting to contribute more. Whether this is through an increase in the auto-enrolment contributions or through voluntary measures, we must make sure that the platform we put in place , is as efficient as it can be.