On the 21st March 2013, a few days after the budget, the FCA published a “Guide to the regulation of workplace defined contribution pensions”.

On the 21st March 2013, a few days after the budget, the FCA published a “Guide to the regulation of workplace defined contribution pensions”.

The document’s mainly about giving pension people confidence that the Pension Regulator and the FCA are friends, that their work “dovetails” with each other (tPR’s jargon) or is “joined up” (FCA jargon). Now we all know that the DWP and the Treasury don’t get on and that their Regulators yap at each other as their master’s dogs, but in this paper the two bodies do seem to have sat down around the same table for the greater good.

I have no doubt that they will be (probably already are) at each other’s throats but in this rare moment of regulatory harmony, some important policy statements emerge.

Take this little nugget

When they choose a pension scheme, employers will not necessarily compare contract-based schemes with trust-based schemes. If employers do compare scheme types it will likely be with help from professional advisers. Many employers, especially smaller ones, may simply accept the scheme they are presented with. The employer may not know whether it is contract-based or trust-based.

This underlines how important it is that the quality of any scheme an employer chooses can be assured regardless of its type.

Or this (which is my desktop screen saver for Q2 2014That last message is going to be on every communication I send to IFAs, accountants, bookkeepers, payroll operatives and journalists talking to employers about auto-enrolment.

So a lot of good came out of the cease fire!

Last week I went to the CIPP’s “Capacity Crunch” event in Covent Garden, keen to talk turkey about how we can get employers to choose their workplace pension – or at least find where there is capacity in the market for them.

To my disappointment, news that “advice to employers on scheme selection is not regulated” had not got as far as the august bodies in the room. Indeed when pressed to confirm the position, the Pensions Regulator looked a little confused himself (albeit it was the wonderful Neil Esslemont who works for the auto-enrolment rather than the workplace pension division of tPR).

So for the avoidance of doubt, let’s get everyone on the same page. Employers can choose from any workplace pension provider offering a qualifying workplace pension scheme (a WSPS). The definition of “Qualifying” is currently quite feeble but will be beefed up with the introduction of minimum quality standards in 2015 and again in 2016 when schemes which are in place but don’t quality will have had to strip out non-qualifying features (commission, AMDs etc).

So with this regulatory easement, we would have hoped by now to have seen some help in place from those in the know, to help small companies to choose a workplace pension. The Pension Regulator and the ICAEW and the FCA and the other august bodies I speak to , tell me that they could not possibly endorse one of the multitude of services available to small employers.

Well I wasn’t expected endorsement, but I was expecting competition! Can someone tell me (other than http://www.pensionplaypen.com) one service that provides online assistance to small companies and their advisers in sourcing and selecting workplace pensions for their staff?

I’m not talking the “give us £5k and we’ll write you a report” merchants. I’m talking about online information such as you’d expect to get when buying a dishwasher or a new car or – if you’re an SME, your next photocopier/payroll software or accountancy service.

There isn’t even a directory of workplace pension providers for you to ring up!

For all the freedom given to SMEs to choose a pension for staff, there is simply no infrastructure with which to do it!

I can phone up NEST or NOW or L&G (and I know a lot of employers do). I may as an accountant or bookkeeper or IFA be able to follow the onboarding instructions on the websites of People’s Pension, Standard Life or Bluesky but I have no way of comparing one from another.

In fact, the ignorance of those organisations staging auto-enrolment from 2015 seems to be matched only by the ignorance of their advisers as to what makes for a good workplace pension.

The absolute folly about this is that all the long term-reward and all the long-term risk rests with the choice of the workplace pensions.

If you choose a workplace pension that consistently underperforms over the next twenty years, your staff might get a pension a third less than if you’d got the decision right. Now no-one can predict performance, but if you as an employer pick a loser and your staff suffer, questions will be asked.

And the first question that will be asked is “why did you choose that dog of a pension boss”.

And if the answer is that it was the one we were “presented” by our adviser, or the one that the Government did or the one we saw on the door of the taxi, then that answer is not going to be good enough.

Because we are not talking any old rubbish here, this is the investment vehicle that your staff are going to rely on for their Lamborghinis, Robin Reliants or more sensibly their top-up income to their state and occupational scheme benefits.

What’s more it is their money and not yours that you’re investing.

So if you can’t come up with a coherent document that properly audits the decision you’ve taken, you are going to be found wanting if (and lets hope it’s not a when) you’re workplace pension is found wanting.

It’s not an issue of regulation- it’s an issue of competence. Sadly there simply is too little competence in the market. Unless you go to a reputable advisor who researches workplace pensions, has the links to the providers to tell you who will offer you (specifically) a workplace pension and has a means to help you compare and choose the workplace pension for your staff, you are on your own. And getting the service outlined above is not cheap, nor is the report that documents and future-proofs your decision.

Nobody is saying that this is a problem (yet). That is because it is not a problem (yet). Up and till now the employers taking decisions on workplace pensions have had an advisory budget. Going back to the earlier gobbet from the FCA

If employers do compare scheme types it will likely be with help from professional advisers.

Many employers, especially smaller ones, may simply accept the scheme they are presented with.

Recent research published by the Pension Regulator confirms the research commissioned by NOW and published on this blog (here). It seems that pension advisers are likely to become less important and reliance is going to switch to accountants, bookkeepers and HR and payroll administrators.

But while awareness and technical capacity amongst such experts is high on the technicalities of auto-enrolment, the research finds ;

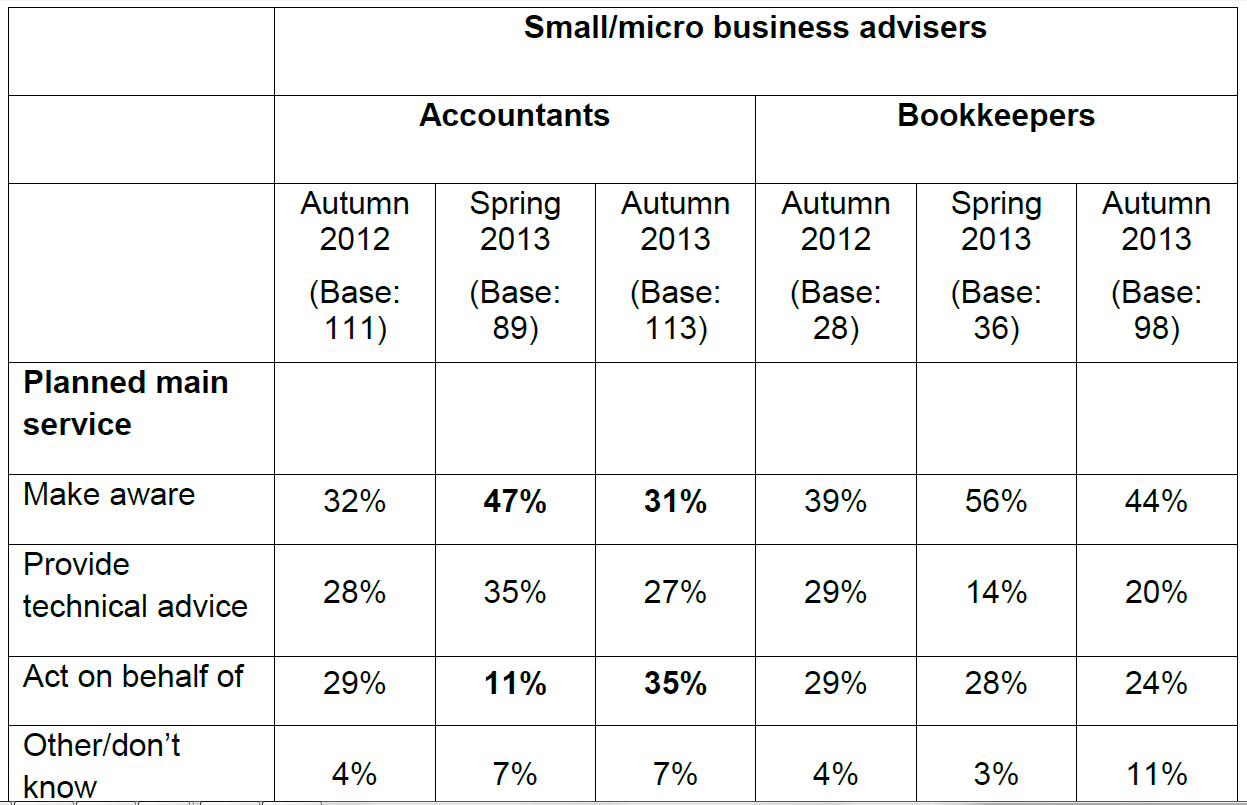

Fewer payroll administrators and HR professionals planned to offer help in choosing a pension scheme (29% and 12% respectively) or reviewing a pension scheme (27% and eight percent respectively).

And it’s not until page 50 that the real meat arrives on the bone. Once we get beyond the in-house experts, there remains the external advisers.

Whereas most small employers are expecting help from their current advisers. these advisers are by and large not planning to be much help! These statistics come from the auto-enrolment division of tPR, asking these questions about the workplace pension, the stats show considerably less

Fewer small/micro business advisers planned to offer help in choosing (35% of accountants and 26% of bookkeepers) or reviewing a pension (33% of accountants and 26% of bookkeepers)

The FCA’s answer to the problem seem to be to rely on the Minimum Quality Standards which have subsequently been published in the DWP’s command paper.

But even with minimum standards in place, there is still going to be considerable variance in the performance of one workplace pension over another.

The durability of many of the propositions we research is virtually zero- a large number of master trusts and some contact based providers do not have credible business plans and without a substantial cash injection or change in strategy, will not survive under the new standards.

Many providers have no game plan to offer the Guidance Guarantee from this time next year and have at retirement options that didn’t pass muster before the budget (let alone when we have Freedom of Choice.

Trying to create a sound rationale for the default investment option (let alone the sub-funds) for most providers is very hard to do. It is hard to see some providers creating credible accumulation strategies (let alone decumulation strategies) within the next twelve months (given that many have paid investment no attention in the past 12 years).

HR and payroll interfaces with providers continue to be a problem. Origo have now given up on creating common auto-enrolment standards for insurers and compatibility between your payroll and HR systems and the providers remains a lottery (there is no definitive matrix for employers to refer to when establishing a plug and play workplace pension.

And communications with staff over what is going on with auto-enrolment, where their money is invested and what options they have to maximise the value of their savings remain at best patchy,

At http://www.pensionplaypen.com, we are saddened by the slapdash way in which employers are choosing workplace pensions and the complacency of their advisers who seem solely intent on selling payroll and HR middleware.

We are saddened too by the lack of engagement with these issues by the major accountancy bodies, ICAEW, ACCA and CIMA. We do not see any appetite among financial advisers to advise on the choice of workplace pensions , nor from accountants and bookkeepers, nor from employers directly.

In short, we see employers walking into workplace pensions without any knowledge of what they are choosing and without advice at hand to make the choice. IFAs are walking away from the pension decision and neither the internal experts or accountants and bookkeepers are intending to help on pension selection.

This is where the real crunch is coming and because we are all so obsessed by the regulations surrounding the auto-enrolment process, we are forgetting that it’s the workplace pension which is what this is all about.

Our website http://www.pensionplaypen.com is a resource for all types of advisers and for employers who don’t take advice. It does the job of finding who will provide pensions to each applying employer , it gives constructive help on which to choose and provides a full audit report on the decision taken. What’s more it does all this in next to no time and for a cost of less than £500.

We need the FCA and the Pension Regulator and the FCA to stay joined up (at least till 2017!) and to start promoting very urgently the need for proactive decision making on the choice of workplace pensions.

We need employers and their advisers to start taking workplace pensions a little more seriously and we really need the FCA and tPR to stay joined up and start promoting the workplace pension decision as critical to the long-term credibility of auto-enrolment

It is simply not good enough to be (to coin the adviser’s phrase) “Provider Agnostic”.

This article first appeared in http://www.pensionplaypen.com/top-thinking

With an online bookkeeper, you are getting a professional that is experienced.

Are You In Trouble With – The IRS or one of the many tax agencies in Washington State.

When looking for accounting software for your business, what features matter most to you.

On the grounds that clerk services are frequently served on an hourly

groundwork, people who work snappier will permit you to recover more.